My book

My book, Designing Data-Intensive Applications, has received thousands of five-star reviews.

Published by Martin Kleppmann on 05 May 2010.

When you’re an entrepreneur out to raise funding, you’re faced with a whole lot of legal and financial jargon, and getting your head around it takes a lot of valuable time – that’s time in which you’re not doing the things which really matter (namely making your product better, making your existing customers happy and acquiring new customers).

But actually, if explained properly, most of the legal and financial stuff isn’t that complicated. The legal documents do a terrible job of explaining, because they define everything in legalese prose. Graphs make it much clearer, as Leo Dirac has shown in his wonderful graphical explanation of liquidation preferences. You should go and look at that presentation.

I’d like to explain a different financial concept, namely the valuation cap on convertible notes. It took me several hours to get my head around it, so I’d like to save you those hours.

The pros and cons of convertible notes

I assume you know what a convertible note (aka convertible loan) is: instead of buying shares in your startup, the investor just gives you the money on a loan with some nominal interest rate. And you promise that when you raise your next round of funding, the loan converts into shares as if they had put that money in during that second round. Since the investor took additional risk by backing you early, they get a discounted share price (they get more shares than someone who puts in the same amount of money in the second round), and that discount is fixed and agreed upon beforehand. It’s typically between about 15% and 30%.

The good thing about convertible notes is that they require less paperwork (and are thus faster to get done), and – in theory – don’t require you to set a valuation, because the share price will be determined in the next round. However, many investors don’t like them. If the company is really successful (as everybody hopes it will be) and the valuation in the next round is high, then the investors don’t get any of that increase in value – they just get their fixed discount, and that’s it.

With some big-name investors, the company’s value goes up simply by being associated with the big name. Naturally, the investor will also want to benefit from that increase in value, because otherwise there’s not much incentive for them to help.

Enter the valuation cap, which appears to now be a standard term of convertible notes, in Silicon Valley at least. The cap is the convertible note investor basically saying: “If things go ok, I’m happy with my fixed 20% discount. But if you do really well, I want us to treat it as if I had bought shares in the first place.” (That way they benefit more from the success.)

So you went for a convertible note hoping that you wouldn’t have to set a valuation for your startup. Well, with the valuation cap you don’t strictly have a valuation, but you do have a range of valuations: the company is certainly not worth less than X, and not worth more than Y.

In effect, someone has now got to decide on a valuation, which is a notoriously unscientific thing. How do you come up with reasonable numbers? You need to somehow build an intuition for what this stuff means.

How to determine your valuation cap

The best way to think about it is to start with some guesswork numbers, consider a range of different scenarios, and work out the consequences. Then you can decide which consequences are unacceptable, and work backwards.

Let’s work through an example. Say you’re a small startup team raising your first seed round, and you expect to raise a Series A from VCs sometime in future. Your input variables are:

There are a few other parameters (like the interest rate on the loan, and the time between the seed round and the series A), but they ought to have only a minor impact.

The biggest unknown here is the amount you’ll want to raise in your Series A, so let’s look at a range of scenarios for that value, and take the other variables to be fixed.

There are two consequences of the numbers which are useful to think about:

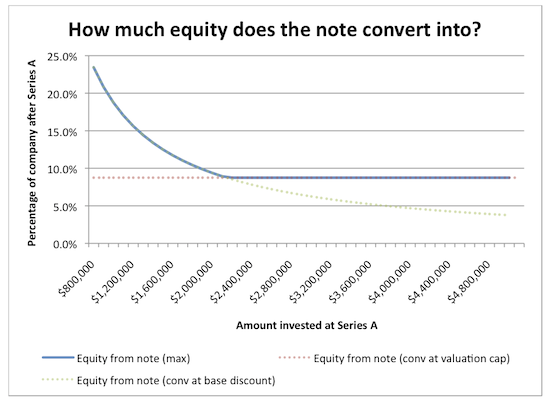

1. What share of the company do the convertible note investors own after the Series A?

We assumed above that after the Series A, the Series A investors own 30% of the company. But how much do the seed investors own after converting their note into shares?

Without the valuation cap, the seed investors end up with an ever diminishing share of the company as the valuation increases. The effect of the cap is that the convertible note investors are guaranteed a certain share of the company, even if you get a Foursquare valuation.

That minimum share is: (1 – [series A investor ownership] ) * [amount raised on conv note] / [valuation cap]. (The first factor takes into account the Series A dilution.) In this example, the note will convert into a minimum of (1–0.3) * $0.5m / $4m = 8.75% of the company’s shares.

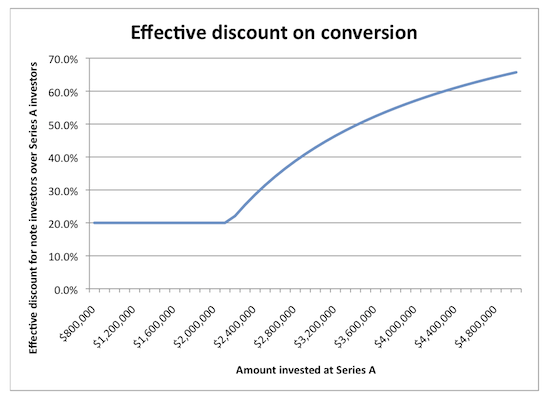

2. What effective discount are the convertible note investors getting relative to the Series A investors?

If you didn’t have a cap, you would simply give a fixed (say 20%) discount when the note converts into shares. But when you have a cap, and your Series A valuation hits the cap, you’re fixing the price for the early investors, while the incoming Series A investors might be paying a lot more per share. So you are effectively giving a greater than 20% discount in that case.

I find this graph interesting, because it’s basically a measure of “how annoyed the VCs are going to be about the convertible note”. – Imagine you’re at the theatre, and you know that for the same ticket you paid 2 or even 3 times as much as the guy sitting next to you. You would not be happy, because it just doesn’t feel fair. If your valuation goes substantially above the cap, there can be a big difference in share price.

Of course, if your startup is awesome and investors are desperate to be part of your round, this probably won’t be an issue. And of course, maybe such a large discount is entirely fair if your Angel investors add a lot of value beyond the money they put in. But it’s a factor to keep in mind. At least with a graph like this you can start thinking about your numbers usefully.

Postscript

None of this gives you an immediate answer to the question “what should we write on our convertible note term sheet?”, but at least you should now be able to think about valuation caps from a few different angles.

Disclaimer: neither am I a lawyer nor do I have much experience with this stuff, so my explanation may be horribly flawed or simply wrong. (If you find a mistake, please let me know.)

You can download the Excel spreadsheet which I used to generate these graphs. An interesting alternative way of looking at this would be to assume a fixed Series A amount, and instead work out what happens when you vary the valuation cap. I’ll leave that as an exercise for you, dear reader.

Incidentally, our awesome startup, Rapportive, is raising a seed round at the moment. It’s filling up quickly, so please get in touch soon if you may be interested. The terms may have certain similarities with my example here, or they may not – I couldn’t say. ;-)

Update (11 June 2010): Packed the Excel spreadsheet in a ZIP file to fix download problems.

Update (23 August 2011): Daniel Odio has made this into a Google Docs spreadsheet – you can just fill in your numbers and see the results immediately. Awesome!

If you found this post useful, please support me on Patreon so that I can write more like it!

To get notified when I write something new, follow me on Bluesky or Mastodon, or enter your email address:

I won't give your address to anyone else, won't send you any spam, and you can unsubscribe at any time.

My book, Designing Data-Intensive Applications, has received thousands of five-star reviews.

![]() Unless otherwise specified, all content on this site is licensed under a

Creative Commons

Attribution 3.0 Unported License.

Theme borrowed from

Carrington,

ported to Jekyll by Martin Kleppmann.

Unless otherwise specified, all content on this site is licensed under a

Creative Commons

Attribution 3.0 Unported License.

Theme borrowed from

Carrington,

ported to Jekyll by Martin Kleppmann.